- agosto 18, 2019

- Posted by: LAS

- Categoría: Uncategorized

SUCCESS CASE

TAX PRESCRIPTION

On this occasion we are pleased to present one of the many tax processes filed by our Firm, in the case of tax prescription for affidavits made by the taxpayer that were not canceled.

Below we briefly narrate the event of the events:

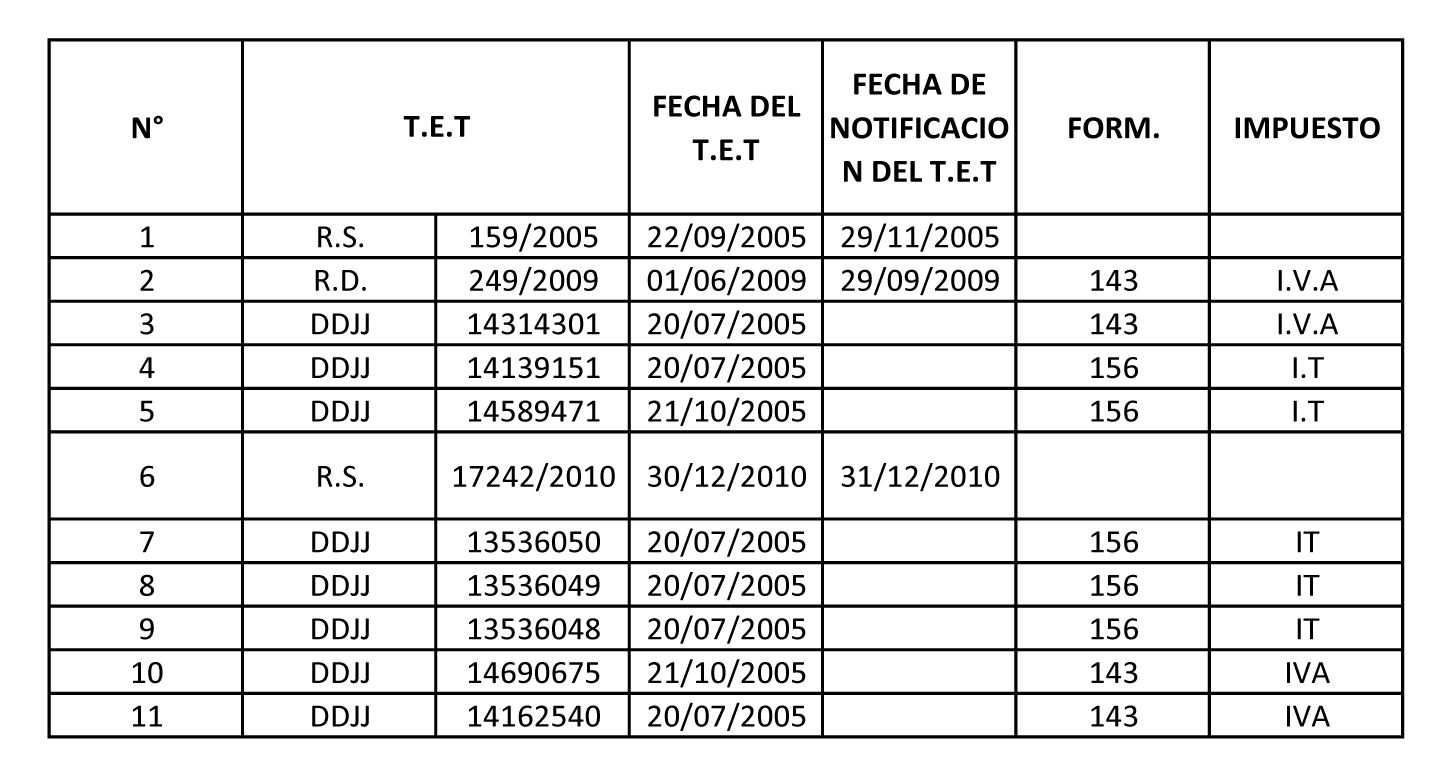

- Our client filed affidavits corresponding to the Value Added Tax (VAT) and Transaction Tax (IT) in the 2004 and 2005 proceedings before the National Tax Service of the Montero Management of the city of Santa Cruz.

- The Tax Administration as a creditor of the tax debt from the date of the sworn statements in the 2004 and 2005 management did not exercise its power of collection, allowing time to pass for more than 4 years as indicated in numeral 4 of article 59 of the Law No. 2492.

- However, despite the knowledge that its faculty of collection was prescribed for the course of time, the Tax Administration proceeded to issue the following Provisions for Initiation of Tax Execution No. 002/2006, 12728/2009, 12867/2009, 12868 / 2009, 12869/20009, 2315/2011 and 71300042915, also proceeding to take coercive measures through the retention of funds, seizure of real estate and others.

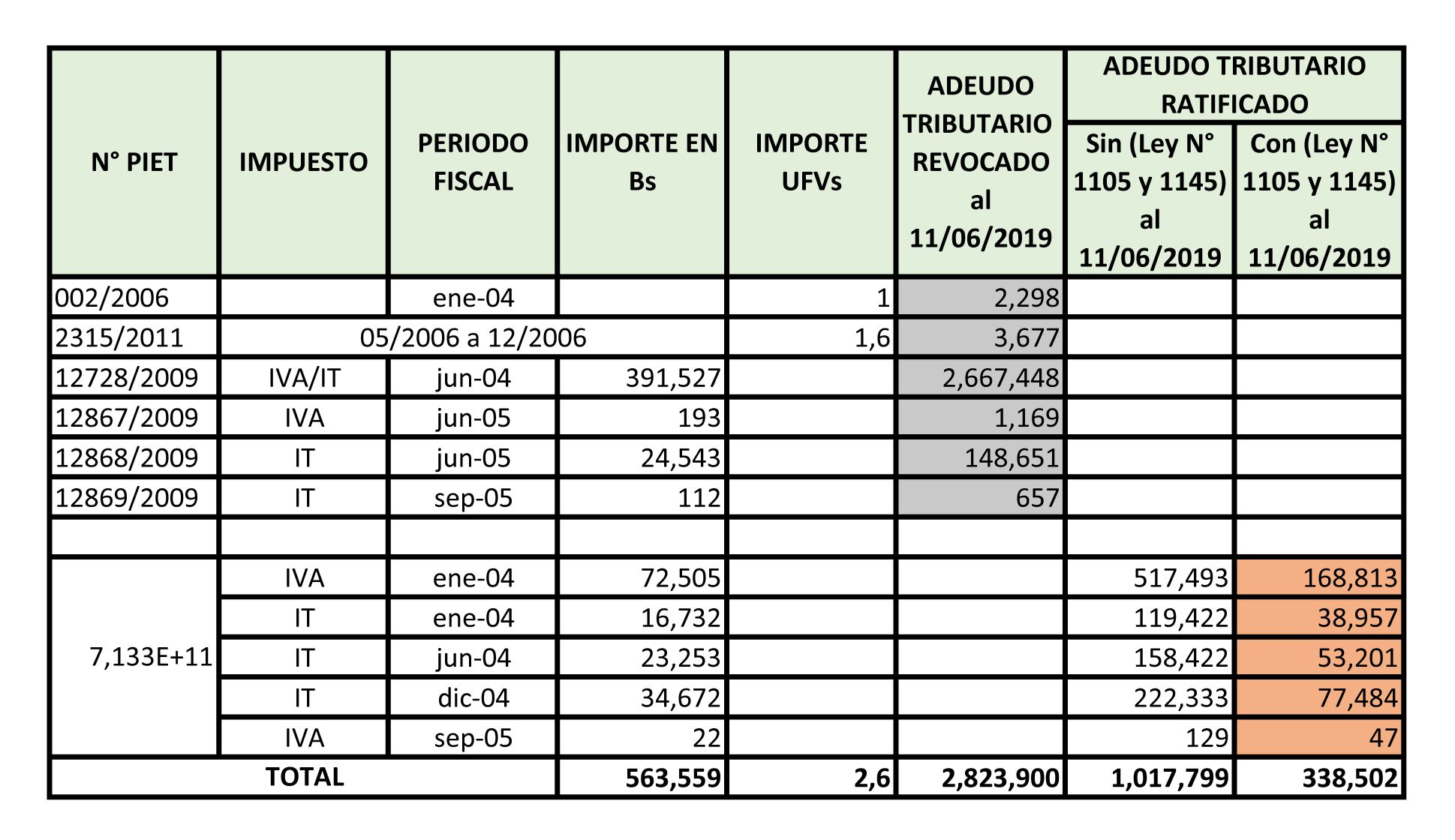

- As a signature, Legal Accounting Services SRL., Once we become aware of this fact, in the 2016 management there was a Tax Prescription incident and after a long pilgrimage in the Montero District Management National Tax Service, despite repeated memorials submitted, two years later they responded to our prescription request by flatly denying it through Administrative Resolution No. 231871000137 with CITE: SIN / GTMR / DJCC / CT / RAP / 00002/2018 dated 11/27/2018, in which it was determined REJECT the Prescription request and CONTINUE with the Tax execution processes until the total recovery of the tax debts that amount to Bs. 563,559 (Five Hundred Sixty-Three Thousand Five Hundred Fifty-Nine 00/100 Bolivianos) and UFV’s 2,600 (Two Thousand Six hundred 00/100 Housing Development Units).

- Once we were notified with Administrative Resolution No. 231871000137, an appeal was filed before the Santa Cruz Regional Tax Challenge Authority, of the following provided for the initiation of tax enforcement

- The Santa Cruz Regional Tax Challenge Authority where, by reviewing the background of the process, the correct foundation and legal defense, we obtained with the Resolution of Appeal ARIT-SCZ / RA 0083/2019 dated March 18, 2019 by which I determine REVOCAR PARTIALLY Administrative Resolution No. 231871000137 declaring the PRECRIPTION of the following PIET´s 002/2006, 2315/2011, 12728/2009, 12867/2009, 12868/2009, 12869/2009 leaving PIET No. 71300042915 in force.

- Hierarchical Resource was filed in part and although the result of the Resolution of the Hierarchical Resource AGIT-RJ 0616/2019 dated 06/06/2019 was to confirm the Elevation Resolution the result remains positive.

PROCESS RESULTS

The tax debt for Sworn Declarations declares and not paid corresponding to the Value Added Tax (VAT) and Transaction Taxes (IT) of the procedures, 2004, 2005 and 2006 updated to the present value in accordance with Article 47 of Law No 2492 CTB amounted to the sum of:

Bs. 3.841,699 equivalent to $us. 551.968,24

Obtaining the declaration of the Partial Prescription, the amount equivalent to:

Bs. 2.823,900 equivalent to $us. 405,732,75

Remaining a balance to pay of: Bs. 1.017,799 equivalente en $us. 146, 235

* That with the benefit of Tax Forgiveness reduced to Bs. 338,502 equivalent to $us. 48,635

– As can be seen from a debt of half a million dollars, the concept of tax prescription was reduced to US $. 48,635.- which means a profit and a tax saving for our client of $ us. 503,333.24.-

This is how the present process is a successful case, in which we managed to reduce considerably the tax debt for the benefit of our client, product of a good technical and legal tax defense, which guarantees our quality of service and prestige as tax specialists.

Click to see the full Hierarchical Resource:

Deja una respuesta

Lo siento, debes estar conectado para publicar un comentario.