- agosto 18, 2019

- Posted by: LAS

- Categoría: Uncategorized

Each year with the new national minimum wage, those achieved with the RC IVA that fill out Form 110 change their amount. In this case for the 2019 management, the National Minimum Wage (SMN) is Bs 2,122.

Through DS 3888 of May 1, 2019, the Executive Branch provides: NEW NATIONAL MINIMUM SALARY – SMN of Bs 2,122.- (Two thousand one hundred twenty-two 00/100 Bolivians); concept that as of May 2019, has EFFECT in determining the tax base and liquidation of the dependent RC-VAT:

- The two (2) SMN, applicable to establish the tax base of the RC-IVA of a dependent, amounts to a maximum of Bs 4,244- (2,122 x 2mn).

- The 13% of two (2) SMN, applicable in the liquidation of the dependent RC-VAT, amounts to a maximum of Bs. 551.72.- (4,244 x 13%).

By means of the RND 101900000010 of June 5, 2019, the National Tax Service provides: ABROG the RND 101900000009 of May 10, 2019, tacitly leaving, without effect, Annex I – Tax Return V.1; Therefore, said rule RULES (again) the application of DS 3890, among others:

- Sending of the Tax Return V.2

- Sending of the electronic information F. 110 presented by the dependents.-

- Presentation of the DD.JJ RC-VAT Withholding Agents Form 608 V.3

- Transfer and use of the balance of the tax credit in favor of the unrelated dependent

- Assignment of “RC-VAT Dependent Code” to each dependent

Comment.- In accordance with Annex I – Tax Return V.2 of the RND 101900000010 in current validity, the columns of “Other Non-Contributing Income” and “RC-VAT Tax of Other Non-Quoted Income” are NO LONGER EVIDENT; understanding that, observations were made through the representations of the unions (College of Accountants, Federation of Factory Workers, Central Workers, etc.), WERE SUBSANATED.

Tax Return V.1. (26 columns) Repeated RND 101900000009

Tax Return V.2. (24 columns) Current RND 101900000010

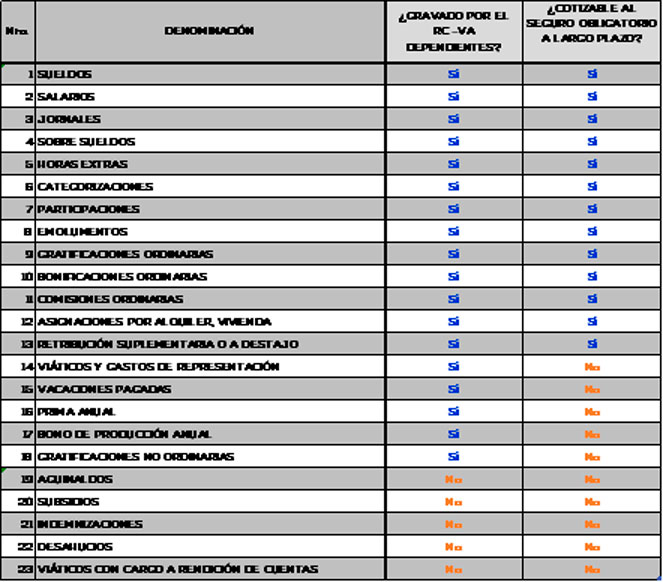

INCOME OF NATURAL PERSONS IN CONDITION OF DEPENDENT EMPLOYEES: For a long time, many of the professionals representing the taxpayers, are not fully aware of which of the income is taxed and not taxed by the RC-IVA, in order to take into account In the application of the income taxed by the RC-VA DEPENDENT and the contributions to the Long Term Mandatory Insurance, we summarize the following summary:

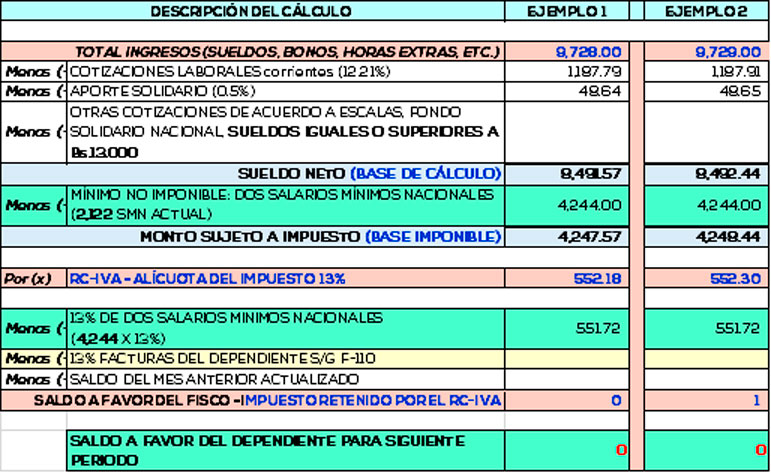

CALCULATION OF RC VAT WITH THE NEW MINIMUM SALARY OF 2019: Below we inform the analysis of the Calculation of RC IVA with the new minimum wage of 2019, also, we complement with the RC IVA Calculator to know how much earning amount is and not necessary submit invoice:

OTHER CHANGES

1.- Generation and assignment of “RC-VAT Dependent Code” to each employee (Art. 8 RND 101900000010 of June 5, 2019).

For this purpose, enter the option “Generation Dependent Code RC-IVA” of the SIN Virtual Office, and register the following information of each dependent:

a) Type of Identity Document;

b) Identity Document Number;

c) Complement of the Identity Document (when applicable);

d) First Surname;

e) Second Surname (when applicable);

f) Names;

g) Date of Birth;

h) Address of Dependent’s Address;

i) Dependent’s Telephone Number;

j) Dependent’s Cell Number:

k) Email (personal).

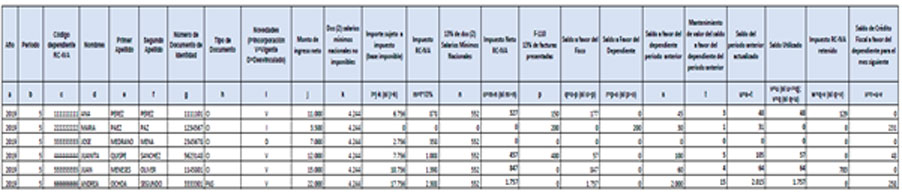

Code that must be registered in Tax Return V.2, as of May 2019

2.- Use of the accumulated balance of the Tax Credit of the unrelated dependent.

The accumulated balance of the Tax Credit of unlinked DEPENDENTS – as of May 2019 -, IS NOT LOST, being able to make use of said balance with maintenance of value in the following cases.

A) Income received after its separation.-

Payments, after the decoupling, for items reached by the RC-IVA, originated in a dependent condition (eg premiums).

The detainee must present “Balance Use Certificate in favor of the RC-VAT Dependent”, which he obtains from the SIN Web Portal, with his “RC-VAT Dependent Code”, this certificate will support the amount to be deducted.

B) Income received on condition of reinstatement

If the detached person was reinstated, and again he is paid concepts reached by the RC-IVA in a dependent condition.

The reincorporated must obtain the “Certificate of Balance in favor of the RC-IVA dependent”, from the website of the SIN, the certificate will establish the balance updated in his favor on the last business day of the month prior to his reinstatement.

Said balance must be registered in the column “Balance in favor of the dependent of the previous period” of the Tax Return V.2 in the fiscal period of its reinstatement.

C) Use of the balance at your next job source

The balance of the RC-IVA in favor of the unrelated dependent may be used by him at his next job source.

The disengaged will obtain the “Balance Certificate in favor of the RC-IVA dependent”, entering the SIN Web Portal, and submit it at their next job source.

3.- Obligation to submit DD.JJ. RC-VAT Form. 608 v.3.

Section e) of Art. 8 of DS 21531, modified by DS 3890 of May 1, 2019

From the fiscal period May 2019 there is OBLIGATION TO SUBMIT MONTHLY DD.JJ. RC-VAT Form. 608 v.3 as a withholding agent for withholding taxes and / or balances in favor of the taxpayer.

Clarify that:

It is important to remember that before the aforementioned modification, there was no obligation to submit DD.JJ., when there was no retention to any dependent.

The information of the Tax Return V.2 corresponding to the month of May 2019 must be presented until the expiration date for the presentation of the Tax Return V.2 corresponding to the month of June 2019 (Transitory Provision – Fourth).

Without another particular we say goodbye to you, remaining at your disposal to answer any questions regarding the case.

Sincerily,

Lic. Rubén Benavides Soliz

Legal representative

Legal Accounting Services

Deja una respuesta

Lo siento, debes estar conectado para publicar un comentario.